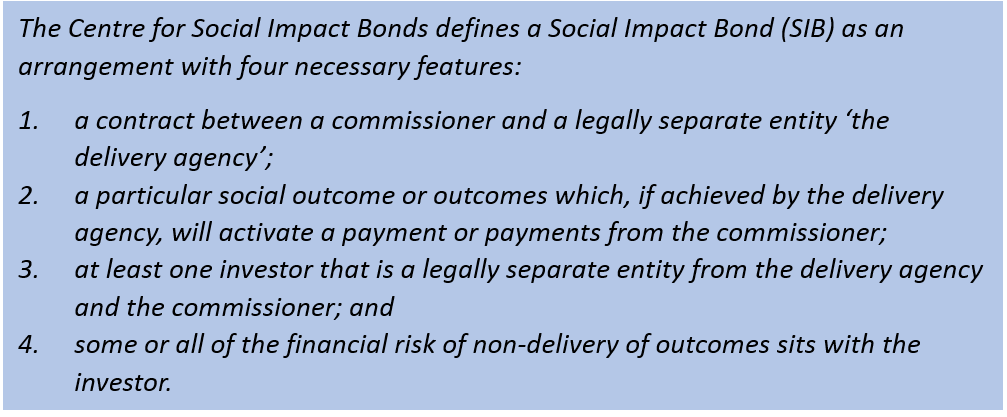

Commercial investors – are they what we’re after?

The Social Market Foundation recently produced a paper titled “Risky Business: Social Impact Bonds and public services” that looked at how to attract commercial investment into Social Impact Bonds. This assumption that commercial/mainstream investors are the ultimate goal for social investment is common, but is made without justification or exploration. Do we need investors who do not value social returns investing in welfare services? A good SIB should be structured so that anyone seeking to maximise their financial return will do so by maximising their social return, but let’s start by having a look at social investors we might have missed out on.

Job applicants and employees are increasingly valuing the corporate social responsibility policies of an organisation. Products that are produced in an ethical and sustainable manner are increasingly in demand, a demand which has not lessened in financial downturn like other premium products. Self-managed superannuation/pension funds are growing in size and number. Are there already a sufficient number of investors who are beginning to say “this is the way I want to invest my money”? Is there scope for allowing these social investors access SIB investments? Can we explore the potential of individual ‘person on the street’ or ‘mum and dad’ investors, often referred to as retail, investors?

Let’s take a look at how SIBs have been sold to investors so far…

Closed, private investments

The 17 investors in the Peterborough SIB and the majority of the other SIB investors in the UK have been found by intermediaries privately, rather than through a public call for investment. Most investors have been philanthropic foundations or individuals. The average investment for Peterborough is around £300,000.

In the US, Goldman Sachs has invested in both SIBs agreed so far. In the New York SIB, the $9.6m investment is part-guaranteed by Bloomberg Philanthropies. In the Salt Lake City SIB their $4.6m ‘loan’ is supported by a $2.4m subordinate ‘loan’ from J.B. Pritzker. (If the intervention fails, the loans will not be repaid.)

Open to wholesale investors

The two Social Benefit Bonds (SBBs) in Australia have raised funds on the open market, resulting in a greater number and range of investors. They have, however, restricted investment to ‘wholesale’ investors. A wholesale investor is a finance professional or a person who has an income of over AU$250,000 per annum for the last two years or assets in excess of AU$2.5 million. An offer restricted to wholesale investors is subject to lower regulatory requirements as it safeguards retail investors from buying products they do not sufficiently understand. The minimum investment for both SBBs was AU$50,000.

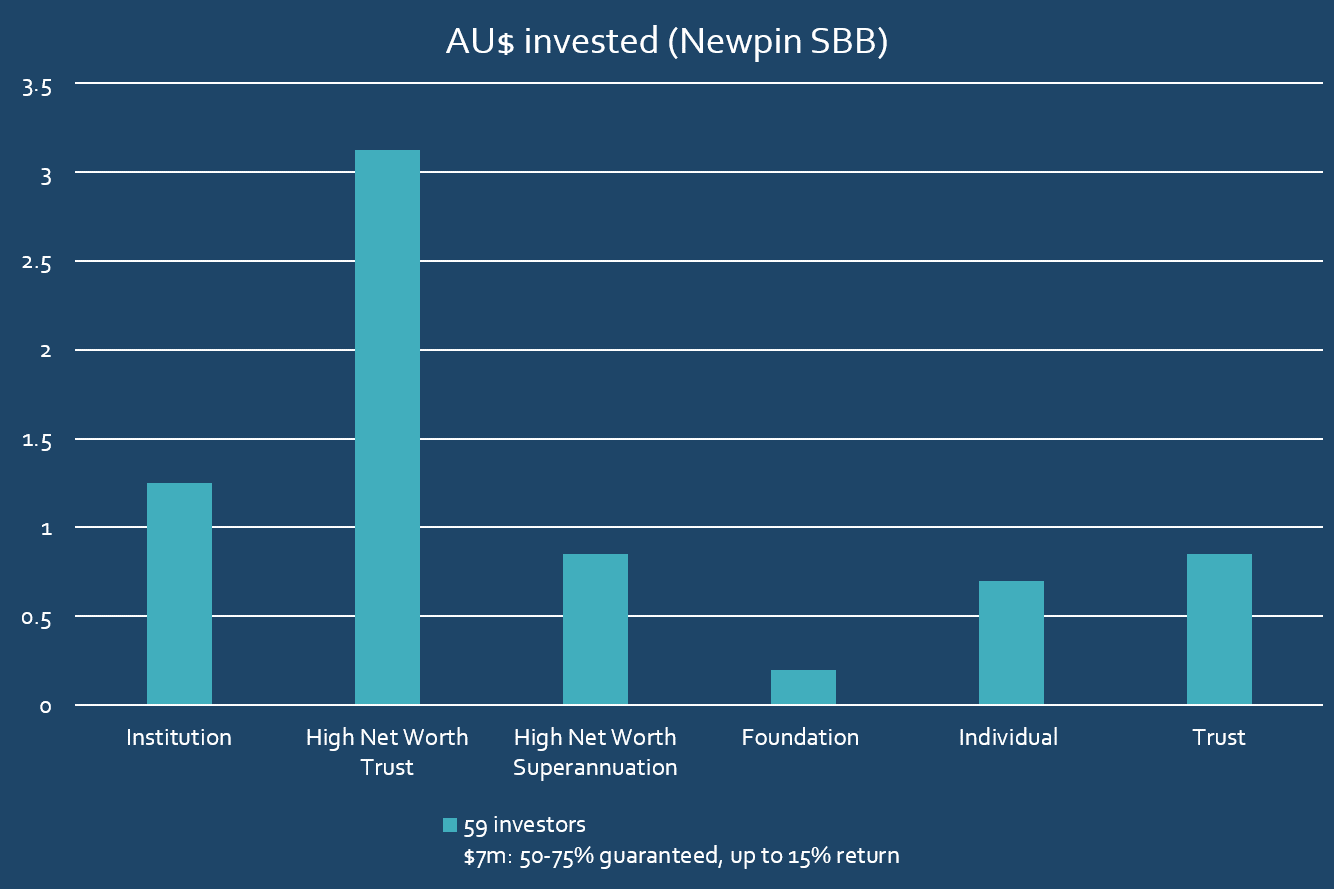

The Newpin SBB was launched first and raised AU$7m from 59 investors. When Social Ventures Australia surveyed investors, 80% of those who responded said they would have invested the money elsewhere if they hadn’t invested in the SBB. Investors included NG Super and Christian Super.

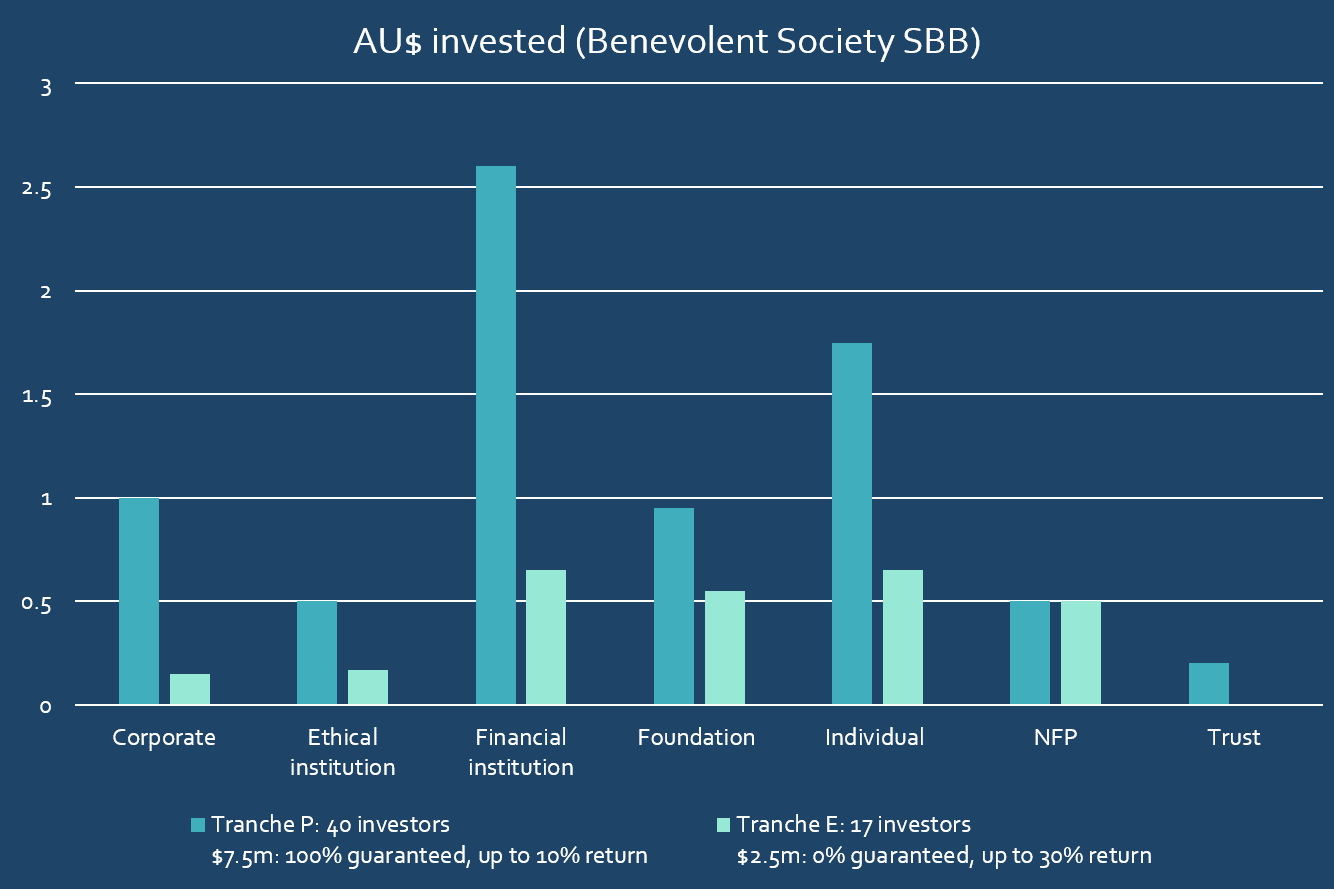

The Benevolent Society SBB raised AU$10m in two tranches. The $2.5m (no guarantee with up to 30% return) tranch involves 17 investors and the $7.5m (capital guaranteed with up to 10% return) tranch involves 40 investors including NRMA Motoring & Services, Australian Ethical Investments and Commonwealth Bank of Australia. Both NRMA and Australian Ethical expressed that while they thought it was a sound investment, this was not a purely commercial investment and the social return was important to them (Australian Financial Review, 5 October).

Smaller, involved investors

The investors in the SIB in Perth, Scotland have contributed between £5000 and £50,000 and are involved in the intervention. Perth YMCA recruited “12 investors – all local businesses or individuals – who were keen to be engaged directly in the delivery of the project, offering their own skills and resources as well as their investment” (Community Links, 2013). This idea of an involved investor in a SIB was unprecedented, but there are many aspects of it that are very attractive. Involved investors have the incentive and the ability to make a real effort to bring about successful outcomes for the young people they’re investing in. It would be interesting to see this model explored in further SIBs.

Service providers as investors

Service providers have invested in their own outcomes in the London Homelessness SIB and in the NSW Benevolent Society SBB. ROCA is also proposing that they invest in the SIB they’re developing in Massachusetts.

Retail investment through a financial advisor

The Allia ‘Future for Children Bond’ was the first opportunity for retail investors to become involved in a SIB. The Future for Children Bond was constructed of 78% loan to a social housing provider, 20% investment in the Essex SIB and 2% management fees. In order to safeguard against ill-informed investor mistakes, the Bond was an ‘advised’ product, which meant that financial advisors had to apply on behalf of investors. The minimum subscription was £15,000. The Bond failed to attract sufficient investment and was closed (NPC, 2013). The Essex SIB is fully funded and operating, with Social Finance, an intermediary, having raised sufficient private investment.

SIBs for the retail social investor?

There is understandable reluctance and legislation against making complex investment products open to individual, retail investors. But the safeguards are not always logical:

- Anyone can give as much as they like to any charity that will accept their donation without scrutiny. And yet if they stand a chance of getting this money back, it becomes an investment and they are subject to heavy regulatory barriers.

- To safeguard investors from making an investment mistake, we set them a minimum amount that they can risk. So they are not allowed to risk $100, but they are allowed to risk $100,000. Might it not be more sensible to safeguard retail investors by setting a maximum amount?

- Commercial investors find SIBs “a difficult investment because it is a small, illiquid product with no credit rating” (Australian Financial Review, 5 October). They understand the way a certain number of products in the market work and to them a SIB is very new. But to retail investors, all investments are to some extent a minefield. Most people will never read all the fine print, but will learn new products and systems as they go. Very few who enter into a mortgage understand all the terms and conditions – a fact exploited and revealed in the sub-prime mortgage collapse of 2008. Crowdfunding is taking off. Retail investors may actually find the SIB less alien and confronting than their commercial counterparts.

Retail investment involves the writing of prospectus documents, which may involve higher transaction costs, but this cost should decrease as more are produced.

In August 2014, I became a retail investor in the Newpin SBB. An original wholesale investor transferred a parcel of investment to me. Australian restrictions around advertising investment opportunities to the open market cease to apply to later, private transfers. I hope that other retail investors will be able to join me in this and other SIB investments soon!