(Source: The Benevolent Society. “First Charity” refers to the Benevolent Society being the first charity established in Australia.)

(Source: The Benevolent Society. “First Charity” refers to the Benevolent Society being the first charity established in Australia.)

On June 14 2013 it was announced that the terms of a second social benefit bond have been agreed in New South Wales, Australia. It will provide services to strengthen 400 families and reduce the need for out-of-home care over five years, beginning October 2013. Press releases were issued by the charity service provider, The Benevolent Society and one of their partners in the SIB, Westpac Institutional Bank. The other partner was a second bank, the Commonwealth Bank of Australia and the involvement in this deal of two of the four large Australian banks has captured media attention. The banks were involved in the construction of the bond as pro bono advisors and are also investors. The Benevolent Society is also investing in the Social Benefit Bond, a move promote confidence in their ability to deliver outcomes. Other investors include institutional investors NRMA Motoring & Services and Australian Ethical Investments.

Investors will provide working capital for the services up-front and the NSW Government will cover all repayments once outcomes have been produced and measured. The social benefit bond also involves financial services firm Perpetual as trustee, a move expected to give investors further confidence in the deal. The role of the intermediary as played by Social Finance in Peterborough and MDRC in New York is not played by any organisation in this arrangement in a comparable way.

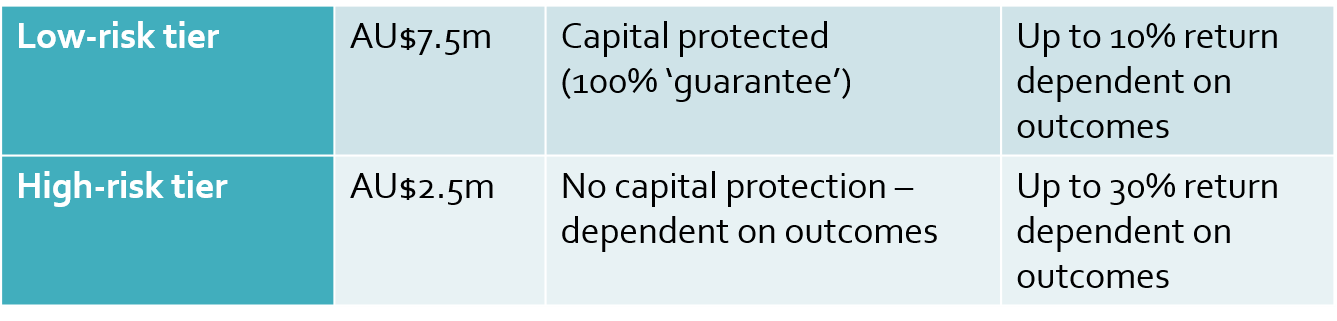

The offering closed on Friday October 4th having raised $10m. 40 investors make up the low-risk tier and 17 investors make up the high-risk tier. In contrast to expectations that social impact bond risk needs to be reduced to attract investors, the high-risk tier proved more attractive and sold out much faster.

Once again, we see the NSW Government offering a guarantee, which means that the Government will pay even if the service does not produce the desired outcomes for recipients. In the previous NSW social benefit bond this guarantee was for between 50% and 75% of investor capital. This time it’s 100% of investor capital guaranteed, but only for the low-risk tier of investments, worth $7.5m or 75% of total investment. This may be an investment by the Government in establishing a market and track record for social impact bonds, rather than a model we can expect to see replicated in future years. The $7.5m of the bond with protected capital will also accrue variable returns up to 10%, dependent on outcomes. An additional $2.5m high-risk tier of investment will involve capital at risk, but will offer outcome-dependent returns up to 30%.

Media Coverage

| Date | Author | Publisher | Title |

| 14/06/2013 | Benevolent Society | First charity issues Social Benefit Bond with Westpac and CBA | |

| 14/06/2013 | Bela Moore | Super Review | Westpac Institutional and Commonwealth team up to launch social benefit bond |

| 14/06/2013 | James Fernyhough | Financial Standard | Big banks move into SBB space |

| 14/06/2013 | Australian Financial Review | NSW strikes deal for $10m social bond | |

| 14/06/2013 | Westpac | First of its kind Social Benefit Bond supports efforts to keep families together – paves the way for socially responsible investors | |

| 15/06/2013 | Clancy Yeates | The Age / Brisbane Times | Lenders back bond to keep children out of foster care |

| 18/06/2013 | Pro Bono | Charity Issues Bank-Backed Social Benefit Bond | |

| 19/06/2013 | Rick Morton | The Australian | Banks pitch in for $10m bond |

| 4/10/2013 | Rachel Alembakis | The Sustainability Report | Westpac, CBA raise $10 million for Benevolent Society SBB |

| 5/10/2013 | Sally Rose | The Australian Financial Review | NRMA and Australian Ethical buy Benevolent Society bond |

This is the second of three social benefit bonds that are the product of a request for proposal issued by the NSW Government in September 2011 and awarded March 2012. The first was the Newpin social benefit bond announced in March and the final bond to reduce adult reoffending is still under development by the Government and Mission Australia, a charity service provider.

(Updated 8 October 2013.)

{kind=link}