Social impact bonds are new, so involve a lot of learning on the job. This learning is less that one SIB ‘works’ and another SIB does not, but more about the iterative adjustments that allow for more effective services, more flexible procurement processes, more alignment of incentives in contracts. One aspect of SIBs that is new for many jurisdictions is long-term contracts. Long-term contracts have many benefits to those delivering and receiving services, but in order to respond to information that comes to light over this time, they must also allow for adjustment and termination.

As its second year draws to a close, investors in Australia’s first social impact bond, the Newpin Social Benefit Bond, have been asked to approve an amendment to its payment metrics, so that they more faithfully reflect success for the children and families it serves.

The reason for this is that the metric rewards investors when children in foster care are restored to their families by the court (“restorations”). When developing the metrics, the breakdown of restorations where children would return to foster care (“reversals”) was discussed, but failed to be written into the contracts. The intention of the metrics is to reward social outcomes with financial return, which means that while restorations should result in payments, reversals should not.

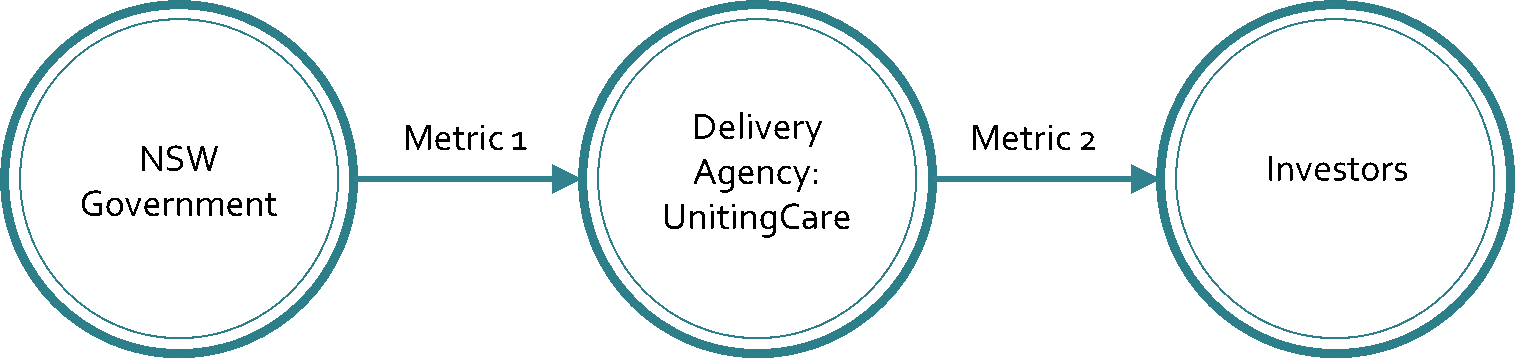

The Newpin Social Benefit Bond has two different payment metrics. One that determines payment from government to the delivery charity, UnitingCare, and a different one metric to determine payment from UnitingCare to Investors.

The problem with each metric and the amendments proposed to rectify these problems are shown below. For original contracts and a more detailed summary of metrics see the bottom of this page.

What is the problem?

- Metric 1 NSW Government => UnitingCare: a drafting error was made that did not deduct reversals in the current measurement period, only previous measurement periods. So the government does not make payments for reversals that occurred in the previous financial years, but does make payments for reversals in the most recent financial year.

- Metric 2 UnitingCare => investors: UnitingCare makes payments based on the cumulative rate of restoration of children to their families. This includes restorations that have been reversed and thus does not faithfully reflect success for families.

In the second year of the SIB, several reversals occurred. So all parties wanted to ensure that these were not paid for in the same way as successful restorations. Government and UnitingCare agreed to amend their metric (Metric 1). An amendment to the investor metric (Metric 2) was also sought to limit payments for unsuccessful restorations. In order to change the metrics, all 60-odd investors had to agree to it. They were also given the option of selling their investment. Using the results to the end of May 2015, the amended metric would return 7.5% interest to investors for the year, while the original contract would return 13.5% interest for the year. If investors did not agree to the amendment UnitingCare would have to pay the inflated interest and continue the service with an imbalance between payments from government and the interest paid to investors. This may have led to UnitingCare exercising their termination rights at the end of year 3. A 10% cap on reversals was proposed in order to limit the ongoing risk to investors and increase the likelihood that they would agree to the amendment.

The proposed amendment

- Metric 1 NSW Government => UnitingCare: change to not paying for reversals that occur within 12 months of a restoration.

- Metric 2 UnitingCare => investors: change to not paying for reversals that occur within 12 months of a restoration, but only up to a cap of 10% of restorations. If more than 10% of restorations are reversed, then reversals over this cap are treated as successful restorations for the purpose of calculating the interest paid by UnitingCare to investors.

The amendment still leaves us with an imperfect metric.

- If the proportion of reversals is above 10%, UnitingCare will make interest payments to investors (based on the cumulative restoration rate) which will include restorations that have been reversed, even though this does not reflect success for the families involved.

- If the proportion of reversals is above 10%, UnitingCare will make a success payment to investors that includes reversals over the cap, but for these reversals, UnitingCare will not receive government outcome payments.

- There were no reversals in the first year of the SBB and 28 children were restored from the mothers’ centres. In the second year to May 2015 (not a full year), 20 children were restored from the mothers’ centres, and 7 of these restorations were reversed, some being reversals of restorations from the previous year. The reversals at the mothers’ centres represent 15% of cumulative restorations. Therefore reversals for the second year are above 10% of restorations. If the amendment is agreed and applied retrospectively to year two, UnitingCare will pay investors for restorations that were not maintained, and for which they themselves receive no payments.

What can we learn?

There are several key lessons I draw from this experience. Note that every other stakeholder may have a completely different list!

- It’s important to be able to learn as you go and respond to new information, allowing for amendments, dispute and termination on fair terms.

- Having different metrics determining payments to the delivery agency and payments from the delivery agency means that there is some misalignment of incentives.

- The Newpin SBB has a mix of ‘impact-first’ and ‘finance-first’ investors. The 10% cap was a way of striking a balance between them. While the fiduciary duties of those investing through structures such as self-managed super funds and Private Ancillary Funds do not conflict with them making social/impact investments, some perceived agreeing to a lower rate of return as conflicting with their fiduciary duties as trustees.

- When contracting for outcomes, enormous attention has to be paid to thinking through all potential scenarios, however unlikely, to ensure the intended social outcomes are reflected in the legal terms.

- It is very difficult to reflect the journey of someone through social service systems with a binary measure. The definitions and metrics deem the program as either successful or unsuccessful for children and their families, with no ability to accommodate degrees of success or episodes of care over time.

Update on results to July 2015 (2.25 years of service delivery and second payment to investors)

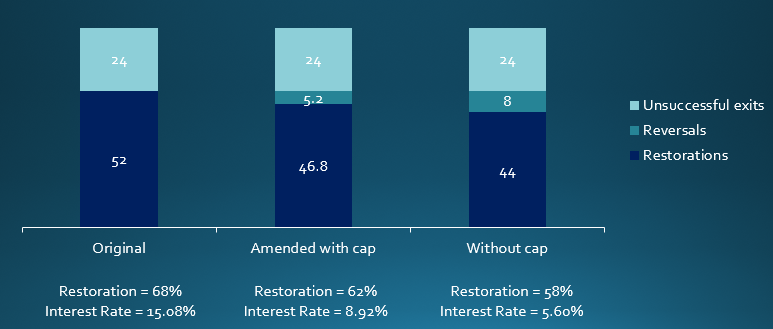

The amendment was passed by all investors. Without the amendment, the Restoration Rate would have been calculated at 68% and the Interest Rate at 15.08%. With the amendment, the Restoration Rate was calculated at 62% and the Interest Rate paid to investors was 8.92%. If there had been no cap, and all reversals were considered unsuccessful outcomes, the Restoration Rate would have been calculated at 58% and the Interest Rate would have been 5.6%. So the investors did agree to forgo much of the interest that was due to them under the original agreement, but gained over 3% more than if all reversals were treated as unsuccessful outcomes. The difference in the investor interest was paid by the charity UnitingCare. The amount they were paid by NSW Government paid was not affected by this.

References

- Newpin SBB Amendments Supporting Information June 2015

- Newpin SBB Information Memorandum April 2013

- Deed of Implementation for Newpin Social Benefit Bond (Government-UnitingCare agreement)

Metrics summary

*Note that investor payments relate only to Mothers’ Centres as they were considered lower risk at the time the metric was developed. The discussion above focuses on Mothers’ Centres only. |

Disclaimer: Emma is a retail investor in the Newpin Social Benefit Bond. She bought her parcel from a wholesale investor when the restrictions around types of investors expired. She firmly believes that Newpin does wonderful and important work with families.

[…] Changing A SIB Metric Mid-Flight Emma Tomkinson […]

The investor group were being asked to accept a 6% downgrading on returns, did they agree?

All investors have agreed to the interest downgrade (which may include one or two agreeing to be bought out instead).

[…] one of its metrics ‘mid-flight’ has provided a learning opportunity, as Emma Tomkinson outlines. The problem was that “when developing the metrics, the breakdown of restorations where […]