There was no hype before the Social Impact Bond (SIB) was announced – this is in contrast to other Governments who have announced their intention well before finalising details. Perhaps the deal was developed quickly, which may well be the case with Bloomberg controlling both the philanthropic guarantee and political appetite. Or perhaps the parties didn’t want to announce before they had signed the contracts, avoiding the pressure of having to live up to an announcement of intention.

There was no hype before the Social Impact Bond (SIB) was announced – this is in contrast to other Governments who have announced their intention well before finalising details. Perhaps the deal was developed quickly, which may well be the case with Bloomberg controlling both the philanthropic guarantee and political appetite. Or perhaps the parties didn’t want to announce before they had signed the contracts, avoiding the pressure of having to live up to an announcement of intention.- In addition to a press release, the City of New York released a briefing pack outlining the justification, partners, program and payment terms of the SIB. The terms of Government payment are clearly set out, unlike in the Peterborough SIB. For a new funding mechanism, this certainly promotes understanding.

- It’s called a Social Impact Bond- Obama’s administration announced funding for “pay for success” bonds and the NSW Government has branded them Social Benefit Bonds. Using the same term as Peterborough makes it clear that they follow the same model and helps keep related literature together.

- Bloomberg Philanthropies guarantees it – they’ve only guaranteed $7.2m of the $9.6m Goldman Sachs investment, but having the guarantee reduces investor risk and may be one of the key factors in getting this deal finalised. It’s not clear under what terms the guarantee is paid or what happens to it if it’s not required. The fact that it’s a grant seems to suggest that MDRC would repurpose it. This also means that like Peterborough, if outcomes are not achieved, there is no payment of public monies.

- The Goldman Sachs payment to MDRC is described as a loan – people often ask of SIBs “Are they debt or equity?”. In fact, they are neither, they are multi-party contracts. Payments from Government are due to an outcomes-based contract. The private investor is really buying a futures option. Classification as debt sheds light on how Goldman Sachs will account for this investment. It also may suggest that Goldman Sachs will take a hands-off approach. If this is so, the benefit of investor skills and incentive are not transferred through to the service providers. This transfer has historically been referred to as one of the reasons for involving external investors, but we’ve yet to see a SIB where investors have a relationship with service providers.

- Similar to Peterborough, there is a third-party, independent evaluator. This may prove to be an essential feature of all SIBs as they emerge.

- The intermediary is MDRC, a research centre – the strengths of MDRC are in program evaluation and design. Intermediaries in other SIBs bring financial investment or service delivery experience to the SIB. In NSW, the intermediary role will be played in part by banks and not-for-profits, as well as by the intermediary Social Finance (no relation to the UK or US Social Finance).

- The payment terms state that a 10% reduction in recidivism is the threshold for investors to break even, although when cost of capital is factored in, this will represent a loss. It is not clear what the 10% reduction is in relation to i.e. what the comparison group is. The SIB also uses stepped payment terms, rather than a sliding scale, which is simple and unambiguous.

- There is value in being a first mover – the press releases announces the “Nation’s First Social Impact Bond Program”. There is a conflict between the kudos received for being a first-mover and the confidence gained by waiting to see how other SIBs turn out. It will be interesting to see whether SIBs become more popular and mainstream, or whether development of this model will slow once its novelty wears off.

- Benefits to nonprofit providers are described in the briefing pack as “a committed funding stream not subject to budget cuts”. The literature that exists on SIBs describes the major benefit to be providers being the flexibility afforded by focusing on outcome, rather than current prescriptive Government contracts. This could be a sign that MDRC will be prescriptive in what it asks of the two providers, or that prescriptive contracts are less of an issue in this jurisdiction.

- Is there conflict between innovation and evidence? The briefing pack justifies the SIB as “encouraging innovation in a time of fiscal constraints”. The idea that SIBs encourage innovation by allowing Government to pay only if outcomes are achieved might be one for the long-term market only. At the moment, the reputational risk of failure to all parties and intense media scrutiny has resulted in SIBs providing services with a strong history and evidence-base that may require strict adherence to service models. These services are so safe they would be ideal candidates for a direct outcomes-based contract with a provider. The real innovation occurring here might be in how the delivery partners have to work together towards agreed outcomes.

- They’re creating a pipeline – the press release refers to an August 2 request for expression of interest for additional social impact investment projects by the City of New York. This would suggest that a pipeline of proposals will be established, but I haven’t been able to find the request anywhere. It would be interesting to see whether outcomes are suggested and priced, in the manner of the NSW Government, or whether this will be up to the market.

social impact bonds

NPC on payment by results and unneccessary complexity in charity contracts

Two fantastic new blog posts – I feel a bit like an NPC groupie, but I can’t help it when they produce such great work!

David Pritchard’s post is about the sector response to the Ministry of Justice payment-by-results proposals with a link to the report out of their workshop. The report lays out the stakeholder perspectives and the ‘key principles’ really nicely – clear and concise. Most of the issues are similar to what we’ve come across in Social Benefit Bond developments, but they organise it well and it’s always good to get perspective on the same issues being from elsewhere.

Iona Joy posts on the complexity of contracts and how developing tendering departments may not be something we want charities to do! She compares her experience with long, arduous contracts as a banker to the simpler ones of venture capital.

How do you know when outcome change can be attributed to your intervention?

It was exciting to read the new working paper Addressing attribution of cause and effect in small n impact evaluations: towards an integrated framework by Howard White and Daniel Phillips. While it would be ideal that all the interventions we design would have the number of participants (n) and impact that would give us a statistically significant result at a high level of confidence, there are many reasons that this doesn’t happen. For payment-by-results contracts, in particular social impact bonds, attributing an impact to an intervention is a pre-requisite for the transfer of public funds. Also, funders the world over are attempting to identify the impact they are making across their portfolios, to increase the effectiveness of their investments. White and Phillips produce a fantastic summary of methods and examples that seek to attribute change to a cause. While their framework of small n methods is useful, it’s their up-to-date literature review that I find most useful.

It was exciting to read the new working paper Addressing attribution of cause and effect in small n impact evaluations: towards an integrated framework by Howard White and Daniel Phillips. While it would be ideal that all the interventions we design would have the number of participants (n) and impact that would give us a statistically significant result at a high level of confidence, there are many reasons that this doesn’t happen. For payment-by-results contracts, in particular social impact bonds, attributing an impact to an intervention is a pre-requisite for the transfer of public funds. Also, funders the world over are attempting to identify the impact they are making across their portfolios, to increase the effectiveness of their investments. White and Phillips produce a fantastic summary of methods and examples that seek to attribute change to a cause. While their framework of small n methods is useful, it’s their up-to-date literature review that I find most useful.

The paper is published by 3ie: International Initiative for Impact Evaluation. 3ie have developed a database of policy briefs, impact evaluations and systematic reviews. They’re governed and staffed by a trans-global team, and while focussed on international development, their evaluation work is certainly relevant for interventions that alleviate disadvantage at a local or national level.

How do we get super funds involved in social investment?

In Australia, superannuation funds are large and growing, so they’re the ideal social investors of the future. But super funds are also highly regulated and risk averse. And rightly so – we don’t want fund managers taking huge risks with our super! So there are two options. Firstly, we can lower the risk of social investment products to suit the requirements of funds. Secondly, most superannuation funds offer their clients a choice of options with different risk and return profiles. There’s an opportunity here to allow clients to chose to invest a portion of their super in social investment options, although we may not quite be there yet…

Phillipa Yelland’s article in today’s Investor Daily, Jury still out on Social Benefit Bonds, questions whether Social Benefit Bonds are good investments, interviewing Nick Ryder from NAB and Peter Murphy from Christian Super. Ryder neatly summarises the SBB concept and notes that we’re looking at a class of investment that do “not necessarily require people to choose between being a philanthropist or an investor”.

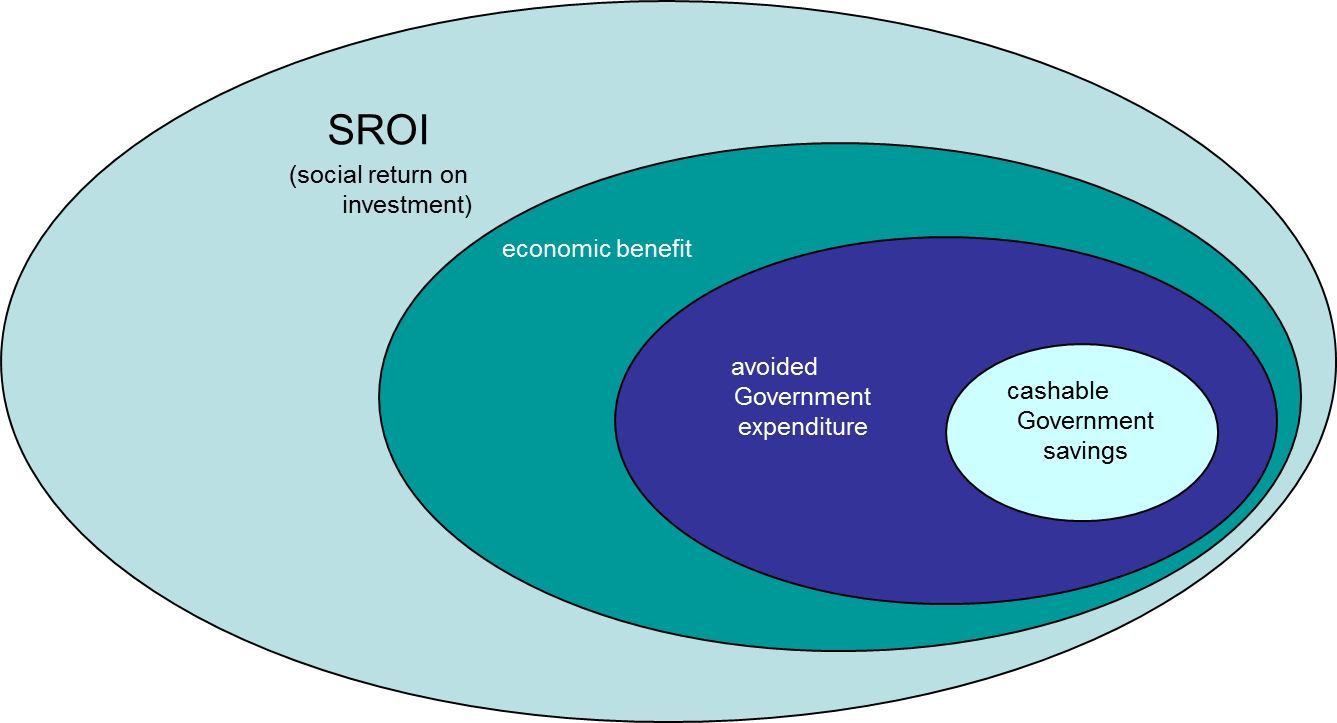

Murphy’s reservations have to do with the SBB’s complexity, the difficulty of understanding the metrics and using Social Return on Investment (SROI) figures. These reservations reflect where the SBB scene is at in Australia right now: we have three SBBs under development in New South Wales, none in the rest of the country, and none operational. We can’t fully understand the risk to investors until the terms, structure and the metrics of the SBBs under development have been decided on. The use of SROI is a separate issue. While it will be useful and meaningful to know the full social return of the SBB investments, returns to investors and Governments are unlikely to be calculated using this method. Investor return depends on outcome change, measured in a way that is closely related to costs Government is able to avoid. SROI itemises outcome change for all stakeholders and gives each of these a value. The basis of an SBB is limited the value of the outcome change for one stakeholder – the Government body funding it.

Will we see more randomised controlled trials in social program evaluation?

Randomised controlled trials are the preferred measurement meth![]() od for the NSW social benefit bond (social impact bond) trials. The Coalition for Evidence-Based Policy published an overview and demonstration of rigorous-but-low-cost program evaluations in March 2012. The publication highlights the use of randomized controlled trials (RCTs) with administrative data systems, providing a number of examples from existing studies. RCTs are widely considered best practice with respect to program evaluation.

od for the NSW social benefit bond (social impact bond) trials. The Coalition for Evidence-Based Policy published an overview and demonstration of rigorous-but-low-cost program evaluations in March 2012. The publication highlights the use of randomized controlled trials (RCTs) with administrative data systems, providing a number of examples from existing studies. RCTs are widely considered best practice with respect to program evaluation.

Omidyar Network to fund social impact bonds globally

Omidyar Network to fund social impact bonds globally

Omidyar Network to fund social impact bonds globally

Omidyar Network announces grants to Social Finance UK and US, but the following exerpt from this article seems to suggest some of the money is destined for Australian social impact bonds!

Omidyar Network’s grants will support the expansion of social impact bonds in the United States, Ireland, Scotland, Australia, Canada and Israel, as well as in the international development sector.

Social Impact Bond Centre for Excellence announced

The UK Government is to set up a new Centre for Excellence to develop more social impact bonds. The announcement appears in this article, but I can’t find the report that is the source…

{kind=link}